ON-SITE MEDICAL CLINICS

Section 49801(d)(1)(B)(i) of the IRS tax code includes on-site medical clinics as applicable coverage under the Cadillac tax, even though it is listed as an excepted benefit under under Section 9832(c)(1)(G).

We recommend that on-site medical clinics should not be considered applicable coverage and are thereby exempt from calculation of the Cadillac tax.

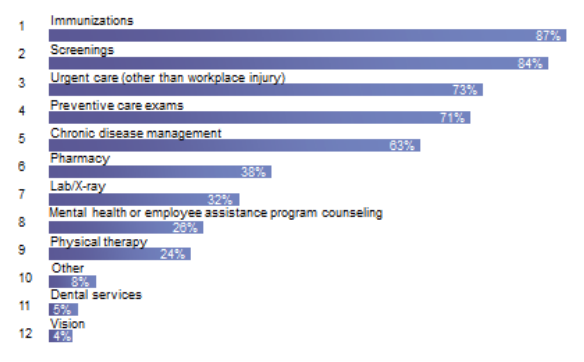

1. Many on-site medical clinics provide services that go beyond the current definition of de minimis care (see Figure 1).

We recommend that on-site medical clinics should not be considered applicable coverage and are thereby exempt from calculation of the Cadillac tax.

1. Many on-site medical clinics provide services that go beyond the current definition of de minimis care (see Figure 1).

Figure 1: Medical Services Offered (based on respondents that have a general medical clinic)

Source: Mercer, "Survey on Worksite Clinics," 2015.

2. Counting on-site medical clinics towards the Cadillac tax will de-incentivize employers to invest in employee clinics and wellness programs, which continue to show positive results.

3. Excluding on-site medical clinics from the excise tax will allieviate conflicting statutory language (in ACA and DOE) that is causing confusion with employers across the country.

4. In rural areas, or Native American reservations, the on-site clinic often functions as employees' primary care if they live in regions where that is the only geographically viable medical clinic. De-incentivizing on-site clinics would cause many employees to lose access to primary care, which opens up concerns for inequity.

5. Calculating the incremental sum of on-site medical clinic towards an employee's premium would be a huge administrative burden.

- 87% employee satisfaction

- 73% clinical utilization

- 63% fewer lost work days

3. Excluding on-site medical clinics from the excise tax will allieviate conflicting statutory language (in ACA and DOE) that is causing confusion with employers across the country.

4. In rural areas, or Native American reservations, the on-site clinic often functions as employees' primary care if they live in regions where that is the only geographically viable medical clinic. De-incentivizing on-site clinics would cause many employees to lose access to primary care, which opens up concerns for inequity.

5. Calculating the incremental sum of on-site medical clinic towards an employee's premium would be a huge administrative burden.

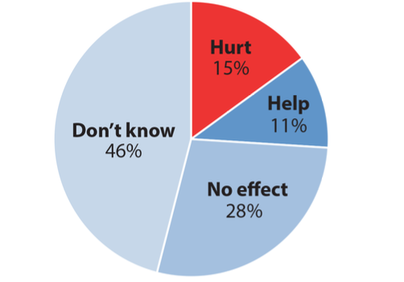

It is imperative that the Treasury and IRS announce further clarify how to define de minimis care for on-site medical clinics because employers are uncertain how to proceed (Figure 2).

Figure 2: Will your clinic help or hurt your Cadillac tax calculation?

Source: Mercer, "Survey on Worksite Clinics," 2015.