|

Currently, in the United States employer-based health insurance plans cover 62% of non-elderly Americans. However, the health insurance industry was not purposefully designed this way. Rather, two fateful twists of history brought us to this current state, and caused a decades-long struggle over controlling costs, expanding access and delivering quality health care.

In the throes of the Great Depression President Roosevelt had an opportunity to pass a national health insurance along with social security. |

Yet lobbying by the powerful American Medical Association threatened to block the Social Security Act of 1935, to which universal health care coverage was linked, and ultimately Roosevelt chose social security over health care. This decision allowed private insurers to fill in the gap, which rise to private health insurance, starting with Baylor University which ultimately became the insurance powerhouse, Blue Cross Blue Shield.

Then in 1942 the U.S. was feeling the effects of a “wartime economy” and in order to prevent inflation, the government imposed wage controls which prevented businesses from competing for scarce workers based on salary. However, the War Labor Board determined that employee benefits, such as health insurance, were to be excluded from wage controls. This gave companies the incentive to expand health insurance and pensions as a way to compete for labor and led to rapid expansion of employer-sponsored health insurance.

Tax policy that favored employer-sponsored plans continued in the decades following the war:

While these decisions were small and piecemeal, over time they had long-echoing effects and now the U.S. faces a $250 billion dollar tax exemption every year for employer-sponsored health plans.

Tax policy that favored employer-sponsored plans continued in the decades following the war:

- In 1949 the National Labor Relations Board ruled that pensions and insurance benefits were considered wages, which meant unions could negotiate benefits packages, including health insurance, as part of their contracts.

- Most importantly, in 1954, the Internal Revenue Service (IRS) decided that employers did not have to pay payroll tax on contributions to employee’s health plans, nor did employees have to pay income tax on their employer’s contributions to their health plans. This meant that the purchase of health insurance for their employees was not taxable, and demand for employer-sponsored health plans further increased.

While these decisions were small and piecemeal, over time they had long-echoing effects and now the U.S. faces a $250 billion dollar tax exemption every year for employer-sponsored health plans.

|

|

|

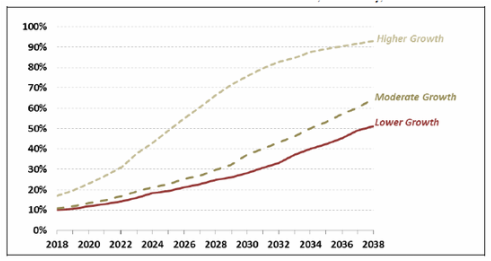

If the tax goes forward in 2020 as it is currently proposed, the initial threshold will be $10,200 for self-only coverage and $27,500 for family coverage. Estimates of how many will be affected vary greatly. The Office of Tax Analysis estimates that 7% of employer-sponsored coverage will be subjected to the tax in 2020. The Congressional Research Service estimated slightly higher results (10.2%) for the first year since it did not take into account those who qualify for higher thresholds. The threshold will increase annually with inflation. Since health care costs are growing at a higher rate than inflation, more plans will be subjected to the tax on an annual basis. It is estimated 24.7% of single (figure 1) and 19.1% of non-single plans will be subjected to the tax (Congressional Research Service).

|

Figure 1: Percentage of employer-sponsored, single premiums estimated to exceed Cadillac tax threshold, nationally, 2018*-2030 (Congressional Research Services, 2015)

Notes: “Lower Growth” scenario assumes annual growth in average health insurance premiums of 4.6%, based on a 5-year average in historical trends; “Moderate Growth” scenario assumes an annual growth rate of 5.0%, based on a 10-year average; and “Higher Growth” estimate assumes an annual growth rate of 7.0%, based on a 15-year average.

*The report was done when the tax was still set to still go into effect in 2018.

Another analysis expects significantly different results than the Congressional Research Service. The Kaiser Family Foundation) predicts that in the first year of the Cadillac tax, 26% of employers will have at least one plan reaching the self-only threshold (includes premium, flexible spending accounts (FSA), health saving account (HSA), health reimbursement arrangements (HRA)). It estimated that 30% of employers will meet the threshold in 2023 and 42% in 2028. The White House refutes these estimates because their analysis focused on employers with at least one plan meeting the threshold where the employee also elected to contribute the maximum contribution to their FSA. In reality, the majority of these employees would not contribute the maximum amount (The Hamilton Project).